Less Rulebook, More Judgement: The New Era of Leveraged Lending Oversight

I wanted to do a special blog piece on the regulatory change (really a rescission) that just occurred about a week ago. Some regulatory events feel like technical edits, and others feel like the removal of a whole reference point. The Office of the Comptroller of the Currency (OCC) published its bulletin 2025-44 on December 5th, 2025. This bulletin, which was transmitted across the country, had an immediate effect on the financial services industry. Written by the OCC and the Federal Deposit Insurance Corporation (FDIC) served to withdraw the 2013 Interagency Guidance on Leveraged Lending as well as the 2014 Frequently Asked Questions (FAQ), were withdrawn. Given the rescission, this regulatory event belongs in the second category of “removal of a whole reference point.”

I want to write this post from not only an informational but also continuing in my “reflective” theme because what matters here is not only what the actual bulletin states, but also what it signals to the market in general, which is already conditioned to learn by constraint. As we know, credit cycles rarely turn because one actor makes a singular “bad” decision; they turn because, across the many desks and committees, the felt cost of saying “no” is rising. Usually, the market discovers late that the underwriting discipline was doing more work than anyone really wanted to admit.

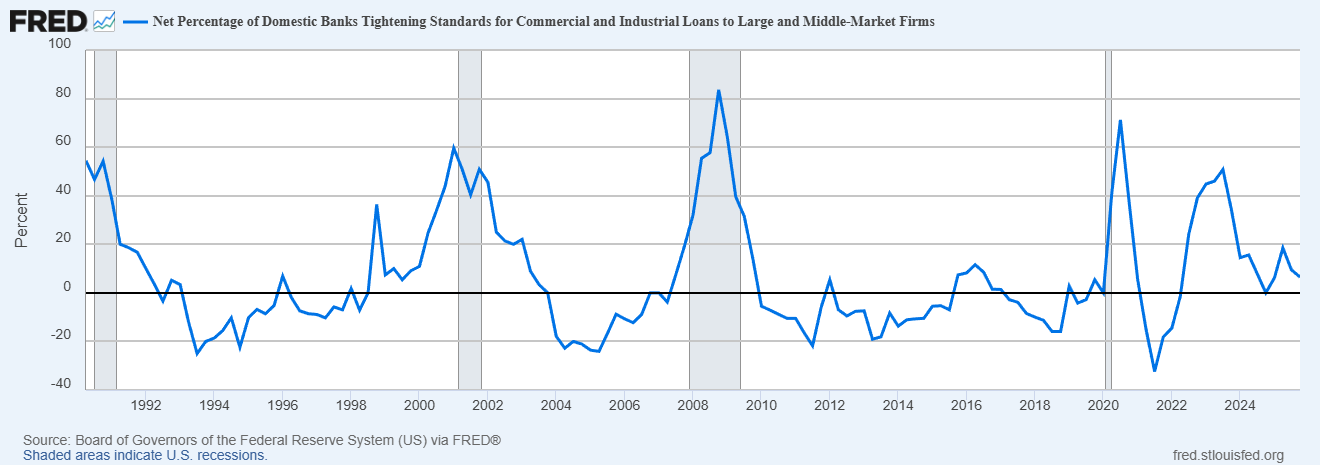

This chart shows whether banks are making it easier or harder for businesses to get loans, when the line is higher, banks are tightening standards, meaning loans are tougher to qualify for.

So, What Changed, Precisely?

In plain terms, the bank regulators took away a specific rulebook that had been guiding how banks should handle “leveraged loans” (loans made to companies that already have a lot of debt). That old rulebook was written in 2013, and it came with extra expectations and tighter scrutiny for these kinds of loans. Now, instead of using that dedicated leveraged-loan playbook, regulators are basically saying:

“Banks should still be careful and responsible, but we’re going back to broader, general safety standards.”

Think of it like this:

Before: “Here are special rules for this high-risk type of lending. You must abide by them.”

Now: “Use the general rules for responsible lending and apply good judgment. Oh, and by the way, we are still watching.”

This does not mean banks can do whatever they want. It implies the oversight is less formula-based and more dependent on whether the bank can justify that the loan was made responsibly.

How can banks be exposed to this risk?

Regulators also clarified that banks can be involved in leveraged lending in two main ways:

1) Direct exposure (the obvious kind)

This is when a bank is directly involved in making the loan, like:

The bank creates a loan for a borrower, and/or

The bank helps sell pieces of the loan to other investors

This is similar to a bank saying: “We’ll help finance this company, and then we’ll share that loan with other investors.”

2) Indirect exposure (the less obvious kind)

This is where non-financial readers usually get lost, so I will do my best to break it down. Here is the simplest version:

Even if a bank is not holding the loan itself, it can still be connected to the risk through the “web” of finance, by financing or investing in other entities that hold those loans.

Examples include:

BDCs (Business Development Companies): These are investment firms that lend to businesses (often to smaller or mid-sized companies).

Debt funds: private funds that lend money to companies outside of traditional banking.

CLOs (Collateralized Loan Obligations): large bundles of leveraged loans that get packaged together and sold to investors—kind of like a “loan mutual fund,” but structured in layers of risk.

The key takeaway for non-finance readers

You all need to know that, if a bank says, “We didn’t keep this risky loan on our books,” the bank itself can still end up exposed to the risk because:

They may have funded the lender who made the loan, or

They may own an investment product that contains those loans, or

They may still be indirectly tied to that borrower through the broader credit system

So, in all cases, the risk doesn’t always disappear; it can just move around the system and sometimes come back to the banks later.

What the old guidelines were trying to prevent.

The 2013 guidance was mainly concerned with more than just leverage ratios. Its main goal was to encourage disciplined financial practices by requiring leveraged borrowers to show they could realistically lower their debt over a set period, typically five to seven years, rather than relying on constant refinancing to support their capital structure.

Ultimately, in the grand scheme of things, this distinction matters because refinancing should not and is not a repayment plan. Refinancing is a market condition. It works beautifully until it does not, and when it stops working, the failure that comes from it tends to be simultaneously spread across borrowers that were all underwritten to the same optimism.

Why do the agencies say they withdrew guidance?

The overall rationale, that I am seeing from the OCC and FDIC, is that the old framework was viewed as being too restrictive, impeding banks’ use of general risk-management principles, and pushed a substantial share of leveraged lending into the nonbank sector, which was outside the regulatory framework or perimeter.

I view this as not a trivial argument. If the so-called activity migrates out of banks and into less transparent vehicles, people may lose visibility, especially when the exposures we talked about are dispersed through funds, securitizations, and bilateral direct-lending arrangements. With that being said, I see the overall trade-off being real; pulling this activity “back” into banks can improve overall visibility, but it can also increase and intensify competition and pressure in a sector that is already highly sensitive to spreads, fees, and sponsor relationships.

Why does the framing matter?

In my eyes, I find the interpretation compelling as it focuses on what often gets overlooked, which is the overall plumbing of the credit market space as a whole. With this being said, how money actually moves, how deals get structured, and how incentives shift once oversight becomes less prescriptive in nature.

If leveraged lending is expected to be managed under the broad “safe-and-sound” principles that the OCC and FDIC want it to be, rather than a dedicated leveraged-loan rulebook, I see several different behavioral outcomes become entirely plausible:

Heavily indebted companies may find it easier to raise funding. We can see this being true as more lenders will be more willing to participate, which will open more channels.

Traditional banks and private lenders are likely to compete more directly for the same deals. This can put overall pressure on pricing and terms.

Deal financing may lean more on short-term “stopgap” solutions and layered capital structures. This will especially be relevant within the mergers and acquisitions space, where speed matters and the buyers want more room to maneuver before locking up their capital permanently.

This lens will be crucial for translating regulatory changes into observable market behavior, such as the speed of risk appetite recovery, shifts in financing terms, and changes in underwriting standards when lenders compete for transactions.

On a related front, we can see that leveraged finance can change direction quickly due to company-specific events. I am reminded of the current major deals that are being contested in the marketplace, such as Warner Bros. Discovery. This new guidance can effectively reshape the entire financial services market, especially the leveraged-loan and high-yield universe. To describe it perfectly, policy sets the boundaries, but deal activity determines how the risk is distributed inside them.

The bigger structural backdrop: private credit scale, bank linkages, and opacity risks.

To understand why both agencies have emphasized “outside the perimeter,” within their statement, we must look at the size and interconnections of the world of private credit.

In May of this year (2025), the Federal Reserve published its “FEDS Note” and estimated that the private credit space was around $1.34 trillion in the U.S. and nearly $2 trillion globally by 2024 Q2. They described it as one of the fastest-growing segments within the nonbank intermediaries. Outside of the Fed, reporting and industry estimates (from S&P Global Market Intelligence) place the private credit space much higher than the Fed’s calculations at about $2.28 trillion. In my opinion, these differences are not contradictory so much as an overall warning; the market is large, growing, and definition sensitive.

Forecast Growth of Global Private Credit AUM (in billions)

A matter of significant consequence for concerns reminiscent of the Global Financial Crisis (GFC) lies in the intricate linkages between traditional banking institutions and nonbank entities. According to a Reuters report referring to research conducted by Bank of America, as of June 2025, shows that banks had extended approximately $300 billion in credit to private credit providers. This development exemplifies how systemic risk may re-enter the financial system through funding mechanisms, even when the underlying loans are categorized as “nonbank” assets.

Reflecting on the story of the 2008 GFC, I believe that it taught a story that crises often travel through funding and liquidity channels, not just through “credit losses” in the narrow sense of it.

Is the GFC analogy appropriate? If so, where it is and where it isn’t.

Leveraged loans are not subprime mortgages; let’s be specifically clear on that, and 2025 is not 2006. The comparison here worth making is not that “this will cause another crisis.” It is way more precise:

Historically and currently, periods of stable credit performance may incentivize procyclical underwriting practices, such as relaxed lending standards, increased leverage, and greater reliance on capital markets for refinancing.

Over time, financial systems are exposed to heightened vulnerability when their stability depends on distribution mechanisms and liquidity sources, including originate-to-distribute pipelines, demand for securitization, and assumptions of short-term funding availability.

Both past and present trends indicate that opacity and complexity within financial frameworks can postpone the recognition of financial stress until it manifests abruptly.

What is important to realize and remember is that the interagency statement itself stresses the risk areas that map to these overall dynamics, which are pipeline controls, refinancing risk over the life of the loan, and independent underwriting, even when buying participations. The agencies are, in effect, saying: “We are removing the old playbook; however, we are not removing the underlying hazards.”

What changes in bank behavior could plausibly follow?

Let’s look at the baseline level and look at incentives. The environment we are in now provides a more discretionary supervisory atmosphere and can produce two very different equilibria:

Equilibrium A: “Better Judgment.”

In response to the regulatory withdrawal, banks may perceive an opportunity to exercise greater discernment in applying core credit principles. This approach enables institutions to develop risk controls that are thoughtfully aligned with the unique attributes of each transaction. Particular emphasis may be placed on assessing the realism of projected free cash flow, strengthening covenant protections, and closely monitoring sensitivity to refinancing risks. Such practices reflect a deliberate shift toward a more nuanced and prudent management of credit exposures, tailored to the complexities inherent in today’s financial landscape.

Equilibrium B: “Competitive Erosion.”

In practice, some banks may interpret the regulatory pullback as permission to aggressively pursue transactions sponsored by private equity or similar entities. This can result in a gradual loosening of underwriting discipline, where banks increasingly rely on optimistic adjustments to earnings before interest, taxes, depreciation, and amortization (EBITDA), accept weaker covenant protections, tolerate higher leverage based on prevailing market norms, and operate under the assumption that capital markets will remain reliably accessible for distributing these loans. Such behavior reflects not only a shift in risk appetite but also an underlying confidence that current market conditions will persist, potentially at the expense of long-term stability.

From my perspective, the second equilibrium is where I see the “Cycle Risk” growing. It does not require recklessness and only involves each desk moving “one inch” to stay competitive in nature, until the industry itself has moved a mile.

This chart shows how nervous or confident credit markets are. When the line rises, investors are demanding extra compensation to lend to riskier companies, which signals higher stress and lower risk appetite.

Where I am seeing potential pressure points and where the “problems” could show up first.

I am watching the following failure modes closely, as they tend to appear before the headlines begin to spike:

Pipeline stress (for non-financial professionals: “hung” syndications).

This is when the markets enter the notion of “risk-off”, banks can get stuck warehousing loans they expected to distribute out to the broader market. This is an overall liquidity and market risk problem before it becomes an apparent credit loss situation.

Refinancing dependence masquerading as repayment capacity.

The more a borrower’s capital structure assumes refinancing as the “exit,” the more sensitive it becomes to rate volatility, spreads, and risk appetite. The agencies explicitly call out refinancing risk as a life-of-loan monitoring requirement.

Indirect exposure surprises (CLOs, BDCs, fund financing).

The statement is explicit that banks may be exposed via CLO holdings or lending to certain debt funds/BDCs. These channels are exactly where “not on our balance sheet” narratives can fail under stress.

Hidden distress in private credit.

BofA research has described private credit as still “fragile,” with default rates around 5% in 2025 and an expectation of modest easing in 2026, while also emphasizing opacity as a vulnerability.

Liquidity mismatch as retail access grows.

The credit rating agency, Moody, has publicly warned about risks associated with rising retail exposure to private credit, particularly where vehicles offer redemption features that can create “run-like” dynamics under stress.

In my opinion, none of these points requires a catastrophe to matter. They are the mechanisms by which credit becomes systemic.

This chart shows the interest rate riskier companies typically have to pay to borrow, when the line goes up, financing becomes more expensive and harder for highly indebted borrowers.

A more comprehensive “watch list” and what I will be putting on my dashboard.

How much debt companies are taking on in new deals

o What this means: Are companies borrowing “a lot,” or “a lot more than usual”?

o Why does it matter: The more debt a company carries, the less room it has to handle bad news (higher interest costs, lower sales, higher input costs).

o Simple analogy: It’s like comparing mortgages; two families might both have a mortgage, but the one with the larger mortgage relative to income is far more vulnerable if layoffs happen.

Whether companies are using “optimistic math” to make the debt look safer

o What this means: Are borrowers or sponsors using aggressive assumptions to make earnings look bigger (so debt looks smaller by comparison)?

o Why does it matter: If the earnings number is inflated, lenders may approve a loan that is actually riskier than it appears.

o Simple analogy: It’s like someone applying for a loan and listing a “future raise” or “possible side hustle” as if it’s guaranteed income.

You’ll often hear EBITDA in these conversations; it’s basically a rough “cash-earning power” measure that lenders use.

Whether lenders are still requiring basic protections in the loan

o What this means: Are lenders still including protective rules, or are they letting borrowers get loans with fewer guardrails?

o Why does this matter: Weaker protections make it harder to spot trouble early and intervene before a situation deteriorates.

o Simple analogy: look at the difference between renting a car with strict rules and inspections versus handing someone the keys and saying, “Just bring it back whenever.”

These are “covenants,” which are rules borrowers must follow (like keeping certain financial ratios or limiting additional borrowing).

What happens to these loans after they are issued (do markets trust them?)

o What does this mean: Are investors treating riskier borrowers differently than safer borrowers, or does everything trade as if it’s equally safe?

o Why does it matter: When markets start “charging more” for risky borrowers (prices fall, yields rise), that’s often an early warning that stress is building.

o Simple analogy: Think of car resale values, if only the “high-mileage, accident-history” cars start losing value quickly, that’s a sign people are getting more cautious.

Many loans trade in markets after they’re made.

CLO activity (bundles of loans sold to investors) and how exposed banks are

o What does this mean: Are these loan bundles easy to sell? Are they offering high returns because buyers are demanding extra compensation? Are banks involved by owning them, funding them, or underwriting them?

o Why does it matter: When CLO demand weakens, it becomes harder to “move” loans out of the system, so risk can get stuck where it wasn’t expected.

o Simple analogy: It’s like a warehouse system. If the trucks stop coming to pick up inventory, the warehouse fills up fast and becomes a problem.

CLOs are large packages of these loans that get sliced into layers and sold to investors.

How much are banks lending to private credit firms?

o What does this mean: Are banks quietly financing the lenders who are making the riskiest loans?

o Why does it matter: Even if banks aren’t holding the loans directly, they can still feel the pain if the private lenders struggle.

o Simple analogy: You might not own the risky business, but if you lent money to the person running it, you’re still exposed.

Private credit firms are non-bank lenders making many of these loans, but banks can still be connected by providing them with funding.

Early signs of distress: defaults, restructurings, and “hidden” trouble

o What does this mean: Are more companies falling behind, renegotiating, or doing “quiet fixes” that delay the moment the market recognizes a real loss?

o Why does it matter: A wave of restructurings can be the “smoke” before the “fire” of higher defaults.

o Simple analogy: It’s like someone juggling credit card payments by transferring balances and extending due dates; it delays the crisis, but doesn’t eliminate it.

A default is when a borrower misses payments. A restructuring is when a borrower negotiates new terms because it can’t meet the old ones.

In summary, my analysis will focus on whether financial transactions are increasingly characterized by higher leverage, optimistic assumptions, and diminished protective measures. Concurrently, I am also examining whether the financial markets and banking sector are becoming more intricately connected in ways that could exacerbate systemic stress during economic downturns.

Closing reflection: the real question is cultural, not technical

I understand the agencies’ motivation to prevent risk from simply migrating out of sight. But the deeper question is whether this withdrawal produces a healthier equilibrium, where banks compete on efficiency and structuring while keeping underwriting intact, or whether it accelerates the most common late-cycle failure, which is the slow normalization of optimistic assumptions.

It is a recurring observation that regulatory safeguards perform their most effective work precisely when their presence remains inconspicuous. Much like a well-placed guardrail on a winding road, their value is most apparent only in their absence. Should these guardrails shift or disappear, the market must then manufacture its own version of discipline, a process that occasionally succeeds, but often requires a costly tuition at the School of Hard Knocks. Ultimately, the ensuing financial "crash course" teaches a valuable lesson: sometimes, the original guardrail was not merely for decoration, but for genuine protection.

Sources:

Berrospide, J., Cai, F., Lewis-Hayre, S., & Zikes, F. (2025, May 23). Bank lending to private credit: Size, characteristics, and financial stability implications. FEDS Notes. Board of Governors of the Federal Reserve System. https://www.federalreserve.gov/econres/notes/feds-notes/bank-lending-to-private-credit-size-characteristics-and-financial-stability-implications-20250523.html?utm_source=chatgpt.com

Federal Deposit Insurance Corporation. (2025, December 5). Interagency statement on OCC and FDIC withdrawal from the interagency leveraged lending guidance issuances (Joint release). https://www.fdic.gov/news/press-releases/2025/interagency-statement-occ-and-fdic-withdrawal-interagency-leveraged

Guevarra, J., & Bharucha, N. H. (2025, November 13). Private credit gains ground among top private equity managers. S&P Global Market Intelligence. https://www.spglobal.com/market-intelligence/en/news-insights/articles/2025/11/private-credit-gains-ground-among-top-private-equity-managers-94290783

Nishant, N. (2025, December 9). US private credit defaults to ease in 2026, but fragility to persist, says BofA. Reuters. https://www.reuters.com/business/finance/us-private-credit-defaults-ease-2026-fragility-persist-says-bofa-2025-12-09/#:~:text=Reuters%20Plus-,US%20private%20credit%20defaults%20to%20ease%20in%202026,fragility%20to%20persist%2C%20says%20BofA&text=Dec%209%20(Reuters)%20%2D%20Private,of%20the%20U.S.%20credit%20market.

Office of the Comptroller of the Currency. (2025, December 5). Leveraged lending: Interagency statement on recission of interagency leveraged lending guidance issuances (OCC Bulletin 2025-44). U.S. Department of the Treasury. https://www.occ.gov/news-issuances/bulletins/2025/bulletin-2025-44.html

Reuters. (2025, October 22). US banks’ surge in loans to private creditors may pose risks, Moody’s says. Reuters. https://www.reuters.com/business/finance/us-banks-surge-loans-private-creditors-may-pose-risks-moodys-says-2025-10-22/#:~:text=Oct%2022%20(Reuters)%20%2D%20U.S.,risks%20if%20underwriting%20standards%20weaken.

Tracy, M. (2025, May 7). Moody’s warns of risk posed by rising retail exposure to private credit. Reuters. https://www.reuters.com/business/finance/moodys-warns-risk-posed-by-rising-retail-exposure-private-credit-2025-05-07/

U.S. Federal Reserve System. (2014, November 7). Frequently asked questions for implementing March 2013 interagency guidance on leveraged lending. https://www.federalreserve.gov/newsevents/pressreleases/files/bcreg20141107a3.pdf

U.S. Federal Reserve System. (2013, March 21). Interagency guidance on leveraged lending. https://www.federalreserve.gov/supervisionreg/srletters/sr1303a1.pdf